THERE MUST BE A GLOBAL MORATORIUM ON RETAIL CBDCS.

For democracies' sake.

Democratic nation states, mysteriously keep having policies pushed upon us that aren’t driven by society and that aren’t overtly by Members of Parliament. They don’t seem really, well, democratic. All too often legislative changes are made with minimal public consultation, and if there is public consultation, it is frequently dismissed or ignored.

My concern rests around the capacity to weaponise smart contracts in the domestic retail sector – households and businesses outside the financial, or wholesale sector. Of course, such functionality would not be toggled in at the start. But there is no doubt that the Reserve Bank of New Zealand has sufficient foresight to predict that (biometrically authenticated) digital identities will likely be toggled to central bank digital currency. A 2020 speech highlighted that:

A CBDC could improve financial inclusion, particularly if it is established with a government-led digital identity scheme.

When democratic institutions and instruments are not sufficiently transparent and accountable. The technical back-end of CBDC functionality will be vastly opaque.

Central banks appear to be trading on present levels of social trust, to provide a social license for progressing with CBDC implementation. But mission creep is eminently possible, particularly when the purposes and functions (and therefore powers) of reserve banks are being expanded, often rather quietly.

Central banks have common policy objectives. However recently many of these policy objectives, or mandates have become looser and broader, more political. We’ve seen recent shifts in New Zealand which have resulted in substantial legislative change over the pandemic period, when the public were distracted.

Democracy relies on the public understanding what is occurring in the hallowed halls and back alley’s of government. But legacy media in New Zealand have predominantly ceased to explore in detail any topic that might contradict government intent.

No public policy wonks have remarked on the remarkable alignment of substantial legislative change that is occurring at precisely the same time that policy on CBDCs is being developed. Over this same period, central bank chatter on the opportunities and technicalities of central bank currencies has soared.

When the institution with the financial and political conflict of interest develops their own principles and sets the rhetorical agenda, they can easily funnel public discourse along a set of rails that fulfil that institutions’ privately held aims.

In 2020 some central banks agreed on ‘three foundational principles’, but the principles don’t revolve around concepts of transparency and accountability, and they’ve been set by the banks themselves, as the Bank of International Settlements Central bank digital currencies: foundational principles and core features paper CBDCs:

(i) do not interfere with or impede a central bank in carrying out its mandate; (ii) coexist with cash and robust private money; and (iii) enable innovation and efficiency in services for end users.

These foundational principles fail to address and deal with pre-existing factors that could very well encourage, or lead to the abuse of power by the banks and their government colleagues. Firstly, degree of power differential, or power asymmetries between the Average Joe on the street and your average central bank, and secondly, the degree to which all information - including decision-making information and programmability, will be secret.

The absence of public debate and legacy media coverage gives us good reason to suspect that that the public remain ignorant of the extent to which CBDC can be programmed and the extent to which the decision-making values and code behind that programmability and smart contracts will be blackboxed.

The functionality will be neither transparent nor accountable. In essence, unlike paper money which of course, cannot be coded, it will be anti-democratic.

But due to the secrecy, the pre-arranged ‘principles’ and quiet arrangements that can be made behind doors, the extent to which we can see that narrative around CBDCs is controlled by the global banking sector, enactment of retail CBDCs should be prohibited.

Indeed, a moratorium should be placed on retail CBDCs.

PROGRAMMABILITY & SMART CONTRACTS

Programmable smart contracts were originally developed as part of decentralised ledger technology (DLT) systems in the financial (wholesale) sector, for very good reason. The smart contracts involved agreements between experts working at a high level. They were reciprocal.

If CBDCs used DLT systems, could potentially promote trust. As Dirk Bullman and colleagues at the European Central Bank stated in 2019:

CBDCs, if they were issued using DLT, could be the ultimate stable asset, enabling funds to be transferred between platforms where crypto-assets are recorded.

However, it’s probably unlikely that CBDCs will be issued using DLT. A Bank of England Discussion Paper stated the following year that:

Although CBDC is often associated with Distributed Ledger Technology (DLT), we do not presume any CBDC must be built using DLT, and there is no inherent reason it could not be built using more conventional centralised technology. However, DLT does include some potentially useful innovations, which may be helpful when considering the design of CBDC. For example, elements of decentralisation might enhance resilience and availability, and the use of smart contract technology may enable the development of programmable money.

By 2016 a flurry of publications were chewing over the technical and legal implications of smart contracts for wholesale payments and crossborder flows. As the Financial Stability Board described in 2017:

Smart contracts are meant to automate the performance of agreements on the basis that any outcome of the smart contract code is necessarily what parties have intended and hence achieve efficiency of contractual performance.

In 2017 the Financial Stability Board was defining smart contracts as “programmable distributed applications that can trigger financial flows or changes of ownership if specific events occur”. Smart contracts can be coded to execute, verify and constrain an action involving either units or representations of assets recorded in a distributed ledger.

If central banks issue a retail digital currency, a retail CBDC, there will be no distributed ledger – decentralised payment system. At this stage it looks like the rules and the algorithms will be set either by central banks themselves, or by the bank in tandem with corporate partners.

Smart contracts (i.e. programmability) on a decentralised system in wholesale/fintech markets are built into legal agreements by mutual arrangement.

However, programmability and smart contracts could be instituted by central banks in retail (i.e. household and business (non financial-sector) situations in a non-agreed, authoritarian manner.

I guess DLT would make it very difficult to centralise smart contracts at retail level.

A 2020 Bank of England Discussion paper acknowledged that:

It is possible to implement smart contracts over a variety of types of ledger, including centralised databases.

It seems more likely is that central banks would operate a core ledger which records the CBDC value and processes the CBDC payments (transactions).

The core ledger would then operate in tandem with (what the Bank of England refers to as) with programmable functionality. Functionalities could be built into the core ledger (by central banks themselves) or be supplied via an Application Programming Interface (API) operated by private sector firms, third-party payment interface providers. Much the same as plug-in modules that enable different functionalities for different purposes.

These (private) interface providers, in sterile banking terms, are imagined to:

provide overlay services that extend the functionality of CBDC.

These services would include advanced functionality that enables programmable money, smart contracts and micropayments which would execute payments based on a predefined criteria. Smart contracts are pieces of code. They could:

be used to automatically execute terms of an agreement, and initiate related transactions, without human intervention.

That Bank of England 2020 paper, that eloquently described programmable money and smart contracts mentioned there could be significant trade-offs. But the Bank of England’s examples focussed on largely apolitical issues such as tax payments or shareholder payments, and electricity meter payments based on use.

But like every paper produced by the International Monetary Fund, the Bank of International Settlements, and by Governors and policy wonks internationally who are embedded in central/reserve banks or monetary authorities – the trade-off of democracy and the undermining of public free will, is not discussed in these papers.

These papers fail to bring attention to, and fail to disclose, the asymmetries of power, conflicts of interest, and what might go wrong.

There will be a wholesale CBDC for big finance, and a retail CBDC for everyone else. Retail CBDCs would ‘meet the payments needs of households and businesses outside the financial sector.’

China is of course leading the way in CBDC implementation. So we can relax.

A BRIEF HISTORY OF CENTRAL BANK CBDC BANKING CHATTER

Digital currencies have been around since 2009, when Bitcoin was privately developed as an internet-based currency and payment system. Bitcoin users have digital wallets and the key innovation that has enabled the technology is a distributed ledger system which enables payments to be made in a decentralised manner.

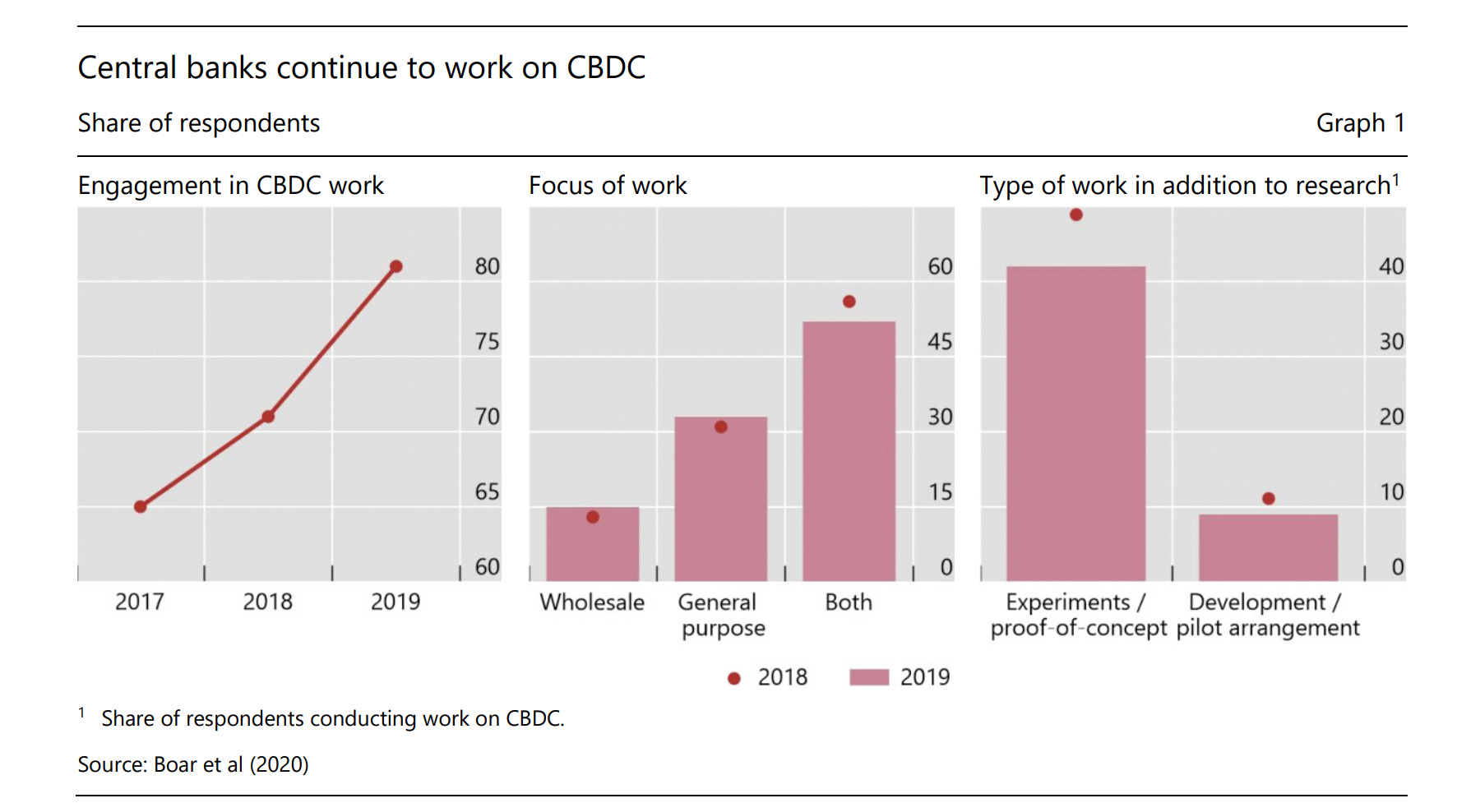

You and your neighbour probably don’t know much about CBDCs. CBDCs aren’t in public chit chat. But CBDCs are giving central banks all over the world, to use colloquial Australian slang, raging stiffies.

The more you understand the extent of cross-talk, the extent of development, the more this appears more like a monetarised digital arms race led by the banking sector, behind closed doors.

The invention of digital currencies and decentralised payment systems presented both a threat and an opportunity to central/reserve banks and monetary authorities. By 2014 the Bank of England (BoE) was publicly speculating that

‘it would technically be possible for an existing central bank to issue digital-only liabilities in a distributed-ledger payment system equivalent to those deployed by recent digital currencies.

By 2015 the Bank’s chief economist was publicly confirming that central bank issued currencies constituted a core part of the BoE’s research agenda. I wondered to what extent the trustworthiness of these technologies were considered a decade ago when the narrative around central bank currencies were being formed. A companion paper hinted that:

With conventional bank deposits, banks hold the digital record and are trusted to ensure its validity. With digital currencies, by contrast, the ledger containing the record of all transactions by all users is publicly available to all. Rather than requiring users to have trust in special institutions, reliance is placed on the network and the rules established to reliably change the ledger.

Yet that paper noted the inextricable social construct, the intangible asset that is a digital currency, or commodity – ‘. Digital currencies have meaning only to the extent that participants agree that they have meaning.’ And that the

‘safeguard offered by digital currency schemes amounts to an undertaking to issue and to recognise new currency only as indicated by an algorithm, which can be amended only with the assent of a majority of computing power on the relevant network.’

By 2016 the Peoples Bank of China governor acknowledged the bank was working on digital currency.

The BIS 2017/2018 Annual Report advised that Morten Linnemann Bech and Rodney Garratt’s Central bank cryptocurrencies paper, published in the September 2017 BIS Quarterly, would outline the taxonomy of money, integrating retail and wholesale CBDs. The Annual Report outlined that in October 2017 the Committee on Payments and Market Infrastructures (CPMI) hosted an industry workshop on CBDCs.

In Chapter V of an associated Annual Economic Report, BIS Economic Adviser and Head of Research Hyun Song Shin discussed in Cryptocurrencies: looking beyond the hype that democratic accountability was key – but accountability needs to be constructed outside bank environments. The bankers themselves are setting the terms of what they reckon accountability might mean.

Soon after a join report was released by the 2018 Committee on Payments and Market Infrastructures Markets Committee Central bank digital currencies discussion which analysed the ‘potential implications for payment systems, monetary policy implementation and transmission as well as for the structure and stability of the financial system’.

Also in 2018, not to be left behind, the International Monetary Fund staff team released the paper, Casting Light on Central Bank Digital Currency, led by Tommaso Mancini-Griffoli.

From European Central Bank board members, to the deputy governor of Japan’s central bank; to the Philippines central bank governor, to the Italian central bank deputy governor, to Singapore’s monetary authority deputy governor, to Mexico’s deputy governor, they’re all chatting about CBDCs.

Then in 2019 the G7 Working Group on Stablecoins - Investigating the impact of global stablecoins looked at them helping understand how they might work:

There are three different types of CBDC that vary depending on who has access and on the technology used (tokens versus accounts). The three types are: (i) digital tokens that can be used by financial institutions (e.g. for interbank and securities settlements); (ii) accounts at the central bank for the general public; and (iii) a digital “cash” token that could be used by the general public in retail payments

In 2018 the former Governor of the Bank of England, Mark Carney gave a talk titled the Future of Money. In December 2019 BIS General Manager Agustín Carstens gave a Princeton University lecture: The future of money and the payment system: what role for central banks?

WHAT CAN WE CONCLUDE?

In April 2018 the Reserve Bank of New Zealand released a bulletin paper outlining digital money, by September 2021 the Reserve Bank of New Zealand was consulting on central bank in a Future of Money consultation. Future of Money is big.

Some key takeaways:

By 2020 the Bank of England had recognised that DLT systems were not necessary, that the Bank would operate the core ledger, and that private firms would develop the functionality behind programmable money, smart contracts and micropayments.

By 2020 central banks had come together the shape narrative around what language would be used to discuss principles, and this language would not involve democratic norms such as transparency and accountability.

There is significant trust that private firms can act as partners, to set the values, the triggers, the coupling devices that households using central bank money would be required to accept.

Banks are trading on existing public trust, but not outlining larger existential risks, such as the potential for abuse of public power, in retail CBDC environments.

A lot happened in the pandemic in New Zealand, that might have missed the public’s notice. By 2020 Christian Hawkesby, Reserve Bank of New Zealand Assistant Governor, in a paper drafted with Amber Wadsworth, discussed the benefits of CBDCs and shared the newly minted Bank of International Settlements three foundational principles for considering CBDCs. Major restructuring of Reserve Bank legislation had quietly occured in 2018, and more would come in 2020-2021, in the middle of the pandemic, when a new bill repealed a large part of the Reserve Bank Act. Only thirty-one submissions were made.

Golly.

But of course, CBDCs will be implemented alongside paper money.

One of the simplest strategies to transfer the population onto central bank platforms will be simply to make the use of paper-based money more inconvenient. As central banks can easily print paper-based money, and they use their own ledgers to create the money, to oversee it, print it and distribute it, paper-based money doesn’t have to be inconvenient. It can be sustained and maintained as a public good.

But this can be made to happen and the public use of paper money can be disincentivise. As former Governor of the People’s Bank of China reportedly suggested in 2016:

Xiaochuan suggested that if its digital currency was phased into the economy, it could become gradually more expensive to transact in paper-based money, thereby motivating users to make the transition.

Right then.

Should there be a moratorium on retail CBDCs?

And the value or worth of this digital fiat token? ...literally nothing. Pull the plug, and it disappears. It's a created illusion to support an illusion of financial value. It defines circular thinking.

As a BRICS currency supplants the petrodollar, the West disappears into its own navel gazing turpitude. One wonders where the righteous screech of citizens freedom groups may be heard? These days it seems a mere whisper downed by dumbed down compliance.